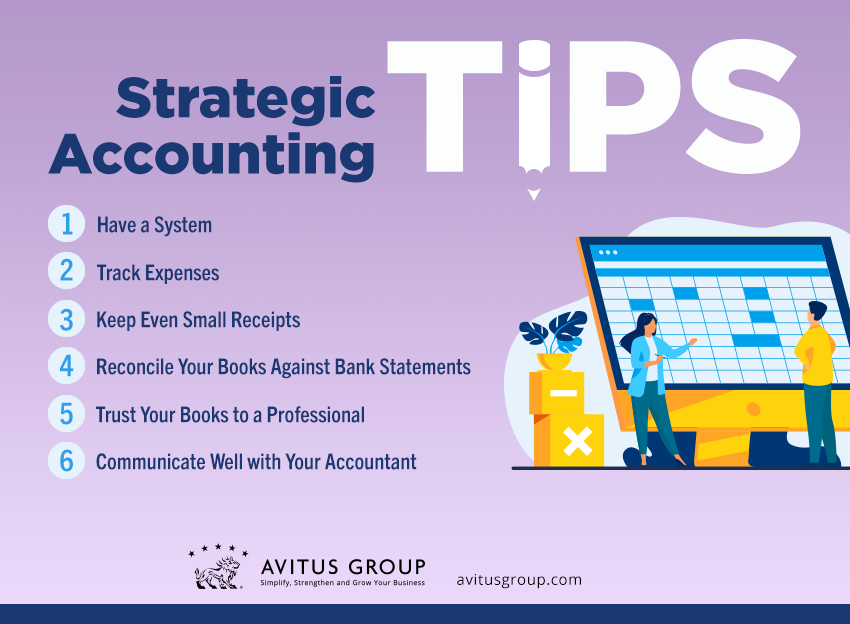

6 Strategic Accounting Tips

Business owners often equate bookkeeping and accounting to housekeeping — administration rather than strategy. But all good accounting is strategic. These 6 strategic accounting tips can make the different between success and failure:

1. Establish an Accounting System

A good accounting system isn’t just stacks of papers, Excel spreadsheets or expensive accounting software.

A proper accounting system is a comprehensive scheme with documented procedures established by an accounting professional. And it operates year-round.

Things can get lost in the cracks, too:

- Employees often don’t keep receipts

- Receipts can get lost before they go into the “shoebox”

- Receipts can get lost somewhere between the shoebox and tax time

2. Track Reimbursable Expenses

As a business owner, you may forget to log expenses for which you use your own money. But those aren’t personal expenses, they’re business expenses. And your company should reimburse you for them.

3. Keep Small Receipts

You may be tempted to throw away receipts under $75, but you should avoid this. Instead, get into the habit of keeping them in one place. You can use these receipts to more easily figure out deductions. Meanwhile, they provide documentation in case of an audit.

4. Regularly Reconcile Books Against Bank Statements

Check your books against your bank statements at least once a month to ensure that small mistakes won’t turn into big ones.

5. Trust the Books to a Professional

In many companies accounting duties fall to whoever is on-hand and reasonably good with numbers.

But that’s a mistake. While you may save money in accountant fees in the short term, your business could lose much more as a result of audits and penalties in the long term.

It’s not the math that can create potential problems — accounting software takes care of much of the numbers. It’s the knowledge of accounting principles and laws behind the numbers.

Accounting software won’t correct:

- Incorrect accounting methods

- Misinterpretation of asset values

- Incorrect estimation of expenses

6. Communicate Well with Your Accountant

Make sure the various departments in your company are communicating with your accountants. Report every financial transaction your company makes, no matter the size.